Note: Please evaluate products before using and investing in them

Why Financial Independence Matters – Now More Than Ever:

Financial Independence (FI) is not just a buzzword. It’s about gaining control over your life. It gives you choices — to change jobs, take a sabbatical, pursue a passion project, or support your family — without being chained to a pay check. Here’s why it’s especially important in today’s world:

Job Security is Fading:

The days of working for one company for 30 years and retiring with a pension are long gone. Today’s private sector is fast-paced, competitive, and unpredictable.

Startups shut down suddenly, even after receiving funding.

Layoffs are common in IT, finance, and even traditional sectors.

Automation and AI are slowly replacing human jobs — from customer service to data entry.

Cultural Responsibilities Hit Early:

In Indian households, the earning members often carry more than just their own financial load.

You may need to support aging parents, siblings’ education, or contribute to weddings and festivals.

There’s also the pressure to buy a house, host a big wedding, or raise children — all while paying EMIs.

Busting Common Myths:

"I need a high salary to get started." ❌

"FI is for older or super-rich people." ❌

"I’ll think about money later." ❌

Reality: It’s not about how much you earn. It’s about how you spend, save, and invest.

From Clueless to Clarity: Start with a Financial Check-In

Before you can build wealth, invest smartly, or make financial plans, you need to understand your starting point. Think of it like using Google Maps — you can't get directions unless the app knows where you are. Financial planning works the same way.

Know Your Ground Before You Grow: Why Financial Awareness Is Step One

Before you dream of financial freedom, early retirement, or investing in stocks and mutual funds, you need to pause and look in the financial mirror. Most people skip this step — and that’s why they stay stuck.

Understanding your current financial situation is like checking your GPS before a road trip. If you don’t know where you are, how can you decide where to go or how long it’ll take?

Let’s break down why this step is absolutely essential:

1. Avoids Blind Spending: Know Where Your Money Goes

You might be earning ₹30,000 or ₹3,00,000 per month — but if you don’t track it, your money can disappear like water in a leaky bucket.

Ever wonder why your bank balance is low despite no major purchases?

Or why you’re always waiting for the next salary to cover basics?

Most people don’t have an income problem — they have a money awareness problem.

Tracking expenses (manually or using apps like Excel) opens your eyes to patterns:

₹200 here on a Food App

₹1,000 there on subscriptions you forgot

₹4,000 every weekend on impulse purchases

Once you're aware, you can fix it. You can’t cut what you don’t know.

2. Helps Set Realistic Financial Goals

It’s easy to say:

“I want to save ₹10 lakhs in 3 years.”

But are you saving anything now? Do you even know how much you can save monthly?

A proper financial assessment tells you:

Your monthly income after taxes

Your fixed and variable expenses

Your existing debt obligations

Your savings rate and investment habits

Let’s say:

Your income is ₹50,000/month

Expenses = ₹35,000

Leftover = ₹15,000/month

You now know you could possibly save ₹1.8 lakhs a year — so saving ₹10 lakhs in 3 years may need increased income, reduced expenses, or a side hustle.

Without clarity, goals remain dreams. With data, they become plans.

3. Prevents Financial Surprises and Panic

We’ve all heard stories like:

“My credit card bill shocked me!”

“I didn’t realize I had that much EMI left.”

“My LIC premium bounced because my account was empty.”

These aren’t emergencies — they’re lack of awareness.

When you take a financial reality check, you become aware of:

Total monthly and annual expenses

Outstanding loans, EMIs, and interest

Insurance coverage and gaps

Irregular but important costs like car servicing, health checkups, gifts, or school fees

This foresight helps you avoid panic, prepare for lean months, and plan in advance.

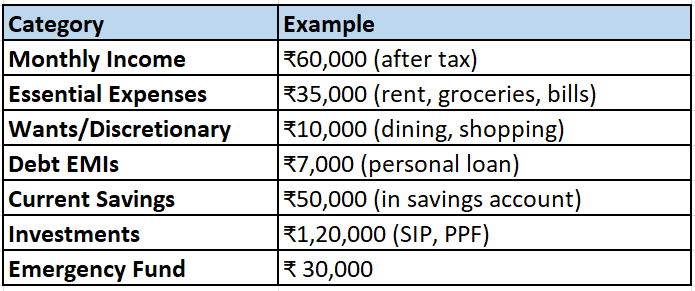

How to Do a Simple Financial Reality Check (Today!)

Here’s a basic framework to get started:

Review this monthly and update it every 3–6 months. It gives you visibility and control over your finances.

Key 3 Easy Steps:

Step 1: Your Wealth Scorecard: Let’s Do the Math

Net Worth = Total Assets – Total Liabilities

Think of this as your financial health report. Here’s how to do it:

List Your Assets (Everything You Own)

Bank savings: Money in your savings/current accounts

Fixed Deposits (FDs): With banks or post office

Public Provident Fund (PPF): Long-term government-backed savings

Mutual Funds/ETFs: Current market value

Stocks & Bonds

Gold: Physical gold or digital gold

Real Estate: Plot, flat, land (only if owned outright)

EPF Balance: Employer Provident Fund

List Your Liabilities (Everything You Owe)

Credit card dues: Outstanding balance

Personal loans

Education loans

Car/vehicle loans

EMIs on electronics or gadgets

Home loan (if applicable)

Step 2: Track Your Monthly Expenses

Most people are shocked when they find out how much they spend on food delivery or subscriptions.

How to Do It:

Use a notebook, Google Sheet, or a mobile app

Step 3: Define Clear Financial Goals

You can’t aim for financial freedom without a map.

Short-Term (0–2 years):

Build an emergency fund

Pay off credit card debt

Save for a new phone/laptop

Plan a trip

Mid-Term (3–5 years):

Buy a vehicle

Save for wedding or post-graduation studies

Build a ₹5–10 lakh savings cushion

Long-Term (5+ years):

Buy a house

Save for children’s education

Achieve early retirement

Build a ₹1 crore+ investment corpus

Each goal should be time-bound, measurable, and realistic.

Example:

Emergency fund of ₹1 lakh in 12 months

SIP of ₹20,000/month in mutual funds to retire by 45

Upgrade Your Mindset, Upgrade Your Money

When it comes to becoming financially independent, your mindset matters more than your income. In fact, how you think about money can be far more powerful than getting a raise. Many people with high-paying jobs still live paycheck to paycheck — not because they don’t earn enough, but because they don’t think like wealth builders.

A strong financial mindset helps you build a foundation that lasts — even through setbacks, job changes, or market dips.

Key Mindset Shifts:

1. From Spending to Investing: Learn to Delay Gratification

We live in an instant-gratification world — one-click shopping, 10-minute deliveries, and EMI offers on everything from mobile phones to furniture.

But the financially wise learn to pause and ask:

“Will this purchase help me reach my goals?”

Instead of spending ₹1 lakh on the latest iPhone, consider:

Investing the same amount in a mutual fund for 5 years

That could grow to ₹1.5–₹2 lakhs — enough for a big goal

“Wealth builders don’t deprive themselves — they prioritize wisely.”

2. From Comparison to Confidence: Escape the Lifestyle Trap

It's easy to feel left out when your friends are:

Booking international trips

Driving brand-new cars

Flashing designer labels

But what social media doesn’t show is credit card debt, empty savings, and financial anxiety.

A wealth builder focuses on long-term peace, not short-term approval.

Instead of saying “I deserve this,” ask: “Does this align with my values and financial goals?”

Confidence in your own path beats constant comparison.

3. Don’t Just Save: Make Money Work for You

Saving is great — but saving alone won't make you financially free. You must learn to:

Invest smartly: in SIPs, ETFs, PPF, NPS, or equity

Plan taxes: Don’t leave it for the last moment every year

Understand returns: A 12% return is better than 4% in a savings account

Wealth builders don’t let money sit idle — they give it a job.

Golden Habits of People Who Build Wealth

Financial independence is not about luck — it’s about daily decisions. These small but powerful habits set the foundation:

Avoid the Latest iPhone EMI Trap

Buying gadgets on EMIs creates a false sense of affordability.

A ₹1.2 lakh phone on 12 EMIs isn’t “just ₹10,000/month” — it’s a liability eating into your future.

Tip: Buy only what you can afford in cash without guilt or stress.

Embrace Budget or Pre-Owned Purchases

When starting out, there’s no shame in:

Using a second-hand laptop

Wearing non-branded clothes

Renting instead of buying

Your goal isn’t to impress — it’s to progress.

Every rupee saved in your 20s can turn into hundreds in your 40s.

Automate Your Savings & Investments

Make saving non-negotiable:

Set up a SIP (Systematic Investment Plan)

Automate transfers to a separate savings account

Treat investing like a monthly bill

When savings happen before spending, your lifestyle adjusts — and your wealth grows silently.

If it’s optional, it won’t be consistent. Automate it.

Budget Like a Boss: Mastering the 50/30/20 Rule (with an Indian Twist)

A great income means nothing if you don’t know where it’s going. Budgeting is the GPS of your financial journey — it tells your money where to go instead of wondering where it went.

Without a budget, even high earners end up broke at the end of the month. With a good one, even modest earners can build wealth.

One of the easiest and most effective ways to manage your money is the 50/30/20 rule. Let’s break it down and then adjust it for the Indian lifestyle.

The Classic 50/30/20 Rule — Simple Yet Powerful

This rule is a basic budgeting formula that divides your monthly net income (after tax) into three clear categories:

50% – Needs (Essentials You Can’t Avoid)

These are things you must spend money on for basic living and survival:

House rent or home EMI

Groceries and household items

Utility bills (electricity, gas, water, mobile, internet)

Commute or fuel

Loan EMIs (education, car, etc.)

Basic healthcare or insurance premiums

30% – Wants (Lifestyle Choices & Fun)

These are non-essential but enjoyable expenses. You can live without them, but they make life more comfortable:

Eating out, Swiggy/Zomato

Netflix, Hotstar, Spotify, etc.

Weekend getaways or vacations

Shopping for clothes, gadgets, etc.

hobbies, events

20% – Savings & Investments (Your Future Self Will Thank You)

This portion builds your wealth and protects you from emergencies:

SIPs (Systematic Investment Plans)

Mutual funds, ETFs

Emergency fund contributions

PPF, NPS, ELSS for long-term growth and tax benefits

Insurance (health & term life)

Indian Reality Check: Adjusting the Rule for Indian Lifestyles

While the 50/30/20 rule is universal, most young Indians (especially in their 20s) live with parents or have shared living costs. This allows for a more aggressive savings approach.

Adjusted Rule for Young Indians Living with Parents:

30% Needs

20% Wants

50% Savings & Investments

Rainy Days Are Real: Building an Emergency Fund

An emergency fund is a financial cushion that prevents debt traps.

Why You Need One:

Sudden job loss

Medical emergencies

Family responsibilities

How Much is Enough?

Minimum: 3 months of essential expenses

Ideal: 6 months, especially if you're the sole earner

Where to Park It:

High-Interest Savings Accounts

Liquid Mutual Funds: Low-risk and better than savings account returns

Short-Term FDs: Easy to break, predictable returns

Avoid putting this money in equity or crypto — it’s not meant to grow aggressively.

Break Up with Your Debt: No More EMI Drama

If you're trying to build wealth but carrying high-interest debt, it’s like trying to fill a bucket with a hole in it. No matter how much you earn or invest, your efforts will keep leaking.

Debt — especially high-interest debt — is one of the biggest obstacles to financial independence.

But the good news? With a clear strategy and a bit of discipline, you can crush your debt and take control of your money.

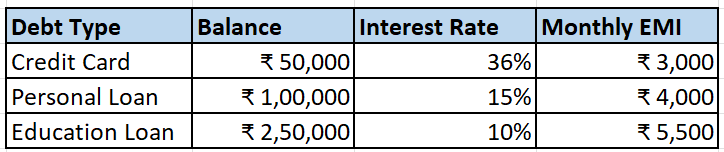

Step-by-Step: How to Tackle Your Debt the Smart Way

Step 1: List Every Debt You Owe

Write down everything — no matter how small.

Credit card balances

Education loans

Home loans

Vehicle loans

EMIs on gadgets or other purchases

Any personal loans from friends or apps

Include the outstanding amount, interest rate, and monthly EMI for each.

Step 2: Rank Your Debts by Interest Rate

Sort your list from highest to lowest interest.

This helps you identify which debts are eating the most into your finances.

Credit cards and payday loans are often the most dangerous, with interest rates as high as 36–48% annually!

Step 3: Choose Your Repayment Strategy

There are two main approaches — both work, so pick the one that suits your personality and situation best:

Avalanche Method (Most Cost-Effective)

Focus on repaying the debt with the highest interest rate first while paying minimums on the rest.

Once that’s cleared, move to the next-highest one.

Saves the most money over time.

Ideal for: People who are motivated by numbers and want to minimize total interest paid.

Snowball Method (Emotionally Rewarding)

Focus on clearing the smallest debt first, regardless of interest.

Once that’s gone, move to the next-smallest.

Builds momentum and gives quick psychological wins.

Ideal for: People who need motivation and want to see faster progress.

Whichever method you choose, the key is consistency.

Common Pitfalls to Avoid

Many Indians — especially early in their careers — fall into these traps:

Swiping credit cards for wants instead of needs

(Think new clothes, fancy dinners, gadgets)Taking personal loans for weddings or international travel

(Your big day shouldn't leave you with big debt)Buying the latest phone/laptop on EMI without real need

(It feels affordable now, but those EMIs eat into your savings)Missing EMI deadlines and paying late fees

(Just one miss can impact your credit score and add penalties)

Pro Tips to Stay Debt-Free:

Set up auto-payments for EMIs and credit card bills — never miss a due date.

Review your debts every 3 months to track progress.

Avoid “minimum due” traps on credit cards — always try to pay in full.

Refinance or consolidate loans if you can get a lower interest rate.

Cut up or pause credit cards if you keep falling into temptation.

Debt gives you short-term joy and long-term stress. Wealth gives you long-term peace.

SIP, Save, Succeed: Investing Tips for India’s New Generation

Start with Mutual Funds via SIPs

SIP = Systematic Investment Plan

Start as low as ₹500/month

Ideal for beginners and salaried individuals

Best Types to Begin With:

ELSS: Tax-saving + equity growth

Index Funds: Low-cost, tracks Nifty 50 or Sensex

Hybrid Funds: Balanced risk-reward

Explore ETFs (Exchange-Traded Funds)

Lower cost than mutual funds

Can buy via demat account (e.g., Zerodha, Groww)

Examples: Gold ETF

Conservative Options

PPF: 15-year lock-in, 7.1% return, tax-free

Learn Before You Leap

Use Zerodha Varsity, ET Money School

Safety First: Demystifying Insurance and Tax for Young Earners

You’re working hard, saving diligently, maybe even investing wisely. But one unexpected event — a medical emergency, an accident, or a job loss — can undo years of progress if you're not financially protected. That’s why smart wealth builders don’t just grow money — they shield it too.

Let’s break it down into two parts: Insurance (protection) and Tax Optimization (savings).

Must-Have Insurance for Every Young Indian

Think of insurance as a safety net — not just for you, but for your family. And no, endowment policies with poor returns don’t count.

Term Life Insurance — Protect Your Loved Ones

Why you need it: If anyone depends on your income (parents, spouse, kids), this is non-negotiable.

How much cover: Aim for 10–15× your annual income. So, if you earn ₹10 lakhs/year, get ₹1–1.5 crore cover.

(Use comparison sites like Policy bazaar or Ditto Insurance)

Health Insurance — Because Medical Bills Can Wreck Your Finances

Even if your employer provides health cover, you still need a personal policy. Why?

Job changes

Layoffs

Pre-existing disease exclusions in corporate plans

Coverage amount: Minimum ₹5–10 lakhs for individuals.

Look for:

No room rent cap (or you’ll pay extra in big hospitals)

Wide network of cashless hospitals

Daycare and OPD coverage, if possible

Consider family floater plans if you're married or have dependents.

Smart Tax Optimization: Keep More of What You Earn

Taxes are unavoidable, but with good planning, you can save a lot every year — legally.

Here’s how:

Section 80C – Claim up to ₹1.5 lakh/year

You can claim deductions for investing or spending on:

PPF (Public Provident Fund) – Government-backed, tax-free interest

ELSS Mutual Funds – Equity-based with a 3-year lock-in

EPF (Employee Provident Fund) – Automatically deducted for salaried employees

Life insurance premium – (Only term insurance, not investment-heavy LIC plans)

Example:

If you invest ₹1.5L across ELSS + EPF in a year, you reduce your taxable income by ₹1.5L.

Section 80D – Health Insurance Premiums

Deduction for health insurance premiums paid:

Up to ₹25,000 for self/spouse/children

Additional ₹25,000 (or ₹50,000 if senior citizens) for parents

Tip: Even if you’re single, paying for your parents’ policy saves tax!

Tools to Make Tax Filing Easy:

"Building wealth without protection is like building a mansion without a roof."

A sudden hospital bill shouldn’t force you to break your mutual funds.

A job loss or accident shouldn’t derail your family’s future.

And tax planning isn’t optional — it’s how you keep more of what you earn.

Shield yourself, save smartly, and let your wealth journey stay on track — no matter what life throws at you.

Final Thoughts

Becoming financially independent in India isn’t just about early retirement. It’s about peace of mind, freedom from toxic jobs, and the ability to live life on your own terms. Whether you’re 21 or 31, the right time to start is today.

Don’t aim to get rich fast. Aim to never be broke again.

Great insights on managing money wisely.